June 15, 2026

By Roland Calia

Executive Summary

Property taxes are the largest single source of state and local government revenue in the United States and are especially important for funding local services such as public education. Their high visibility and sensitivity to rising property values, however, make them politically unpopular, particularly when tax bills increase faster than household incomes. In response, most states have adopted some form of property tax limitation to curb tax growth and provide greater predictability for taxpayers. These policies, including rate limits, levy limits, and assessment limits, are intended to slow the growth of property tax burdens, constrain government spending, and, in some cases, enhance taxpayer accountability through voter approval requirements.

While property tax limitations can provide benefits, including short-term tax relief and budgetary discipline, they also introduce important tradeoffs. Evidence shows that these policies often reduce the rate of growth in property taxes rather than eliminate increases altogether, and their effectiveness varies significantly by design. In Illinois, for example, the Property Tax Extension Limitation Law (PTELL) has not fully achieved its intended purpose due to numerous exemptions and structural features that allow tax growth beyond the nominal cap.

More broadly, property tax limitations can reduce local fiscal capacity, shift reliance to alternative revenue sources, and create inequities across taxpayers—particularly when long-term property owners benefit from preferential treatment relative to newer taxpayers. As policymakers consider reforms, the key challenge is balancing taxpayer protection with the need to maintain adequate, stable, and equitable funding for essential public services.

Strategies to reduce property tax growth and burden in Illinois could include:

- Closing loopholes in tax caps (PTELL) to substantially reduce levy growth

- Applying strengthened PTELL limits to all Illinois counties

- Shifting school funding away from property taxes by increasing state-level funding, paired with mandatory local levy reductions to reset a lower tax base.

- Providing pension parity between the Chicago Public Schools and all other Illinois school districts by shifting funding responsibility for the unfunded liability of the Chicago Teachers Pension Fund to the State of Illinois.

- Reducing the number of taxing bodies to cut duplication and slow cumulative levy increases.

- Limiting unfunded state mandates that drive local property tax increases.

- Tying annual spending increases to inflation or another strict limit to restrain levy growth.

What are Property Tax Limitations?

Property taxes are a primary revenue source for local governments in the United States. In 2023, they accounted for 28.9% of all combined state and local government revenues—more than any other single revenue source. These revenues are collected at the local level.1

Despite the widespread reliance on property taxes, they are particularly unpopular for several interconnected reasons:

- They are based on property values rather than income, so tax bills can rise sharply when assessments increase—even if a homeowner’s income remains unchanged and no property sale has occurred.

- Local governments often impose regular year-over-year increases in property tax levies (the total amount of property tax revenue requested by governments), contributing to a growing burden on taxpayers.

- Many states, such as Illinois, rely heavily on property taxes to fund government services, particularly elementary and secondary education.

These factors tend to steadily increase tax burden, contributing to political pressure to implement policies that freeze or slow the rate of growth in residential and business property tax bills.

Pros and Cons of Property Tax Limitations

Property tax limitations are frequently justified on the grounds that they produce the following benefits:2

- They can enhance stability and predictability for taxpayers by moderating or constraining increases in property tax liabilities over time.

- They can provide property owners with financial relief during periods of accelerated property value growth, thereby insulating households and businesses from sudden increases in taxes owed.

- They can control local governments’ spending and budget growth, especially government entities that are heavily dependent on property tax revenues.

- Requirements for voter approval before implementing tax increases can strengthen accountability by ensuring that tax policy changes reflect public consensus.

However, property tax limitations can also generate a range of fiscal and equity-related challenges:

- They can significantly reduce local governments’ capacity to raise revenue and support services, particularly during periods of inflation, population growth, or increased demand for public services.

- In the absence of property tax revenue growth, governments may shift reliance to alternative taxes that are less stable, less efficient, or more economically distortive.

- Property tax limitations can introduce horizontal inequities in the tax system—meaning unequal tax treatment of similarly situated taxpayers—particularly when long-held properties are assessed or taxed differently than recently sold properties, or when differential treatment exists across property classes.

- Limitations may increase the fiscal vulnerability of school finance systems, especially where funding is shifted toward statewide revenue sources that are subject to political discretion and broader budgetary volatility.

Types of Property Tax Limitations

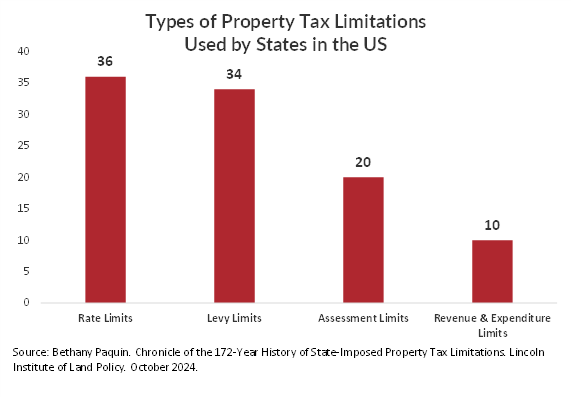

According to the Lincoln Land Institute, a total of 43 states and the District of Columbia impose some form of property tax limitations. The use of these limitations varies across states, with some adopting all of them while others implement only a subset. 3

Rate Limits

A property tax rate is the percentage that a government applies to the assessed value of property to determine the tax owed. It is typically expressed as a percentage of assessed value or as a rate per $100 or $1,000 of property value. A 1% property tax rate means a property assessed at $200,000 would owe $2,000 in property taxes annually.

Rate limits are imposed by 36 states. Rate limits are statutory caps on property tax rates. These limits may fix rates at a set level or restrict their growth over time using an index or formula. They usually apply to specific types of local governments, although in California, they apply to the aggregate statewide property tax rate. Rate limits in Illinois set maximum allowable tax rates for specific funds (such as general operating funds), while some funds, like bond and interest levies, are exempt to ensure debt obligations are fully paid.

Oregon voters approved Measure 50 in 1997, a constitutional amendment that establishes a permanent operating property tax rate limit for local governments. That permanent rate

combines the tax levies that existed locally in 1997. The rates cannot be changed from those 1997 rates. However, voters can approve a “local option levy,” which allows a taxing authority to temporarily exceed the permanent rate limit for five years for operations and 10 years or the useful life of a capital project.4

Levy Limits

A property tax levy is the amount of property tax revenue that a unit of local government or taxing district requests from taxpayers.

Property tax levy limits are legal limits on the amount of revenue that can be raised from property taxes or on the rate of growth in those revenues. A total of 33 states impose levy limits.

An example of a property tax levy limit is Massachusetts’ Proposition 2 ½, which was approved by referendum in 1980. Proposition 2 ½ is both a levy limit and a levy ceiling. The levy ceiling limits local government property tax collections to no more than 2.5% of the fair market value of all property, while the levy limit caps annual increases to 2.5% plus new growth in the tax base. The electorate can override the levy limits through a referendum, in which case the approved override amount becomes the new levy limit tax base.5

Another example of a property tax levy limit is Illinois’ Property Tax Extension Limitation Law (PTELL), often called “tax caps.” PTELL was intended to slow the growth rate of property taxes by capping annual increases in property tax extensions (the total amount billed to taxpayers) for non-home rule governments, such as school districts and park districts, to 5% or the rate of inflation, whichever is lower each year. However, the law contains numerous significant exclusions and exceptions that allow growth beyond the intended limit. For example, growth in the aggregate tax extensions of Cook County governments subject to PTELL far exceeded inflation between 2006 and 2023: property tax extensions increased by 71.3%, while inflation during that period was 46%. In summary, PTELL has not achieved its intended purpose of limiting property tax growth.6

Assessment Limits

Property assessment is the process of assigning market value to properties for taxation purposes. Market value is what the property would sell for in a real estate transaction. Governments can assess property at 100% of the estimated market value or at a percentage of the market value.

Property assessment limits are legal caps on how much the assessed value of property can increase. They can take the form of freezes or increases limited by an index or formula. Assessment limits can be applied to specific local government or geographic areas, or they can be universal limits on all properties. Some states also apply different assessment values to specific types of property, such as primary residences or residential property, and this correspondingly leads to differential tax burdens for different types of property.7 An example would be the Cook County, Illinois, classification system, which assesses residential property at 10% of fair market value and business properties at a 25% rate. Twenty states have imposed assessment limits.

The best-known assessment limit is California’s Proposition 13, approved through a referendum in 1978 as Article XIII A of the state Constitution. Proposition 13 limited the property tax rate to 1% of assessed value at the time of purchase. It also caps annual increases in assessed value at 2% or the rate of inflation, whichever is lower, and generally allows reassessment to market value only when a property is sold or transferred. Certain transfers are exempt from reassessment, including arm’s length transactions with families and transactions involving homeowners over 55 who are replacing their primary residence with a similarly valued property. In addition, Proposition 13 requires a two-thirds vote of the California Legislature to approve state tax increases and a two-thirds vote of local voters to approve special taxes.8

Revenue and Expenditure Limits

Revenue limits are statutory caps on the amount of revenue that can be raised from all sources of revenue in a jurisdiction, including property taxes. They can be paired with expenditure limits.

Ten states impose limits on revenues and expenditures that involve property taxes. In Iowa, Kansas, Nebraska, Minnesota, and Wisconsin, these limits are imposed on school districts. For example, in Wisconsin, school districts may not increase revenues beyond a calculated amount based on prior-year aid, property taxes, and pupil counts. Each school district is allotted a maximum allowable amount of revenue from general state aid and property taxes. If state aid increases, the property tax levy is correspondingly reduced, and total revenue (and hence spending) stays within the cap. The cap can be lifted by a referendum, however.9

In Colorado, the state constitution’s Taxpayer's Bill of Rights (TABOR) limits how much total local government revenue can grow annually by the rate of inflation plus the rate of population growth, unless voters lift those limits by referendum. While TABOR does not directly limit property taxes, governments will often reduce levies or refund excess property tax revenue to stay within the caps the law imposes if property values are rising.10

What Could be Done to Reduce Property Tax Burden in Illinois?

Property tax limitations are intended to slow the rate of growth in property taxes burden. However, in Cook County, despite the presence of rate limits and tax caps on levies (for applicable government entities), property taxes surged 182% in the 30-year period between 1995 and 2024, rising from $6.8 billion to $19.2 billion. This is far greater than the 91% rate of inflation during that period and much higher than the 161% increase in wage growth (161%). The major drivers of this increase are:

- Increases in school district levies, which hiked property taxes by over 189% in this period. In part, this is due to a heavy reliance on property taxes to fund education - roughly 50% of school funding came from local sources in 2023.

- The failure of the state’s property tax cap law to limit tax increases due to myriad loopholes and exemptions. These include levies for certain funds (e.g., some bond funds) and the taxable value for certain property (new property, annexed property, recovered TIF increment, and expired incentive value), which are excluded from the calculation of the PTELL tax cap limiting rate that is applied to levies.

- A multiplicity of local taxing bodies cumulatively and persistently raise levies.

As a result, the total property tax burden has dramatically risen, and taxes are consuming a rapidly increasing share of property owners’ income. Illinois now has the highest effective property tax rate, which is the percentage of a property’s full market value paid annually in property taxes, in the country at 1.83%, according to the Tax Foundation.

What could be done to limit property tax burden in Illinois? There have been proposals to require megaprojects such as the Bears stadium in Arlington Heights to put 50% of special Payments in Lieu of Taxes (PILOT) made to local governments into a fund that would then be divided by 60% toward property tax rebates for homeowners in the megaproject area and 40% into the statewide Property Tax Relief Fund.11 But policies like this are band-aid approaches that would provide minimal tax relief and do nothing to slow the overall rate of growth in levies.

There are, however, several possible strategies to slow the rate of growth or reduce the burden. These are all politically difficult, but worth exploring if policymakers are serious about reducing soaring property taxes. Several of these strategies could be implemented together.

The State of Illinois would necessarily have to play a major role in authorizing and funding solutions. Possible strategies include:

- Eliminate the loopholes in the Property Tax Extension Limitation Law (tax caps), so that levies can only increase by 5% or the rate of inflation, whichever is less, with the goal of instituting a true cap on how much government levies can increase from year to year

- Extend PTELL to all Illinois counties with the elimination of loopholes; currently, only 39 of the 102 counties have adopted tax caps.

- Shift funding for elementary and secondary education from the current heavy reliance on local property taxes to a state funding source and a concurrent mandatory reduction in levies, which would set a new lower base. This would likely require an increase in state resources from income taxes, sales taxes, or the imposition of a state sales tax on services to compensate for the loss of local revenues.

- Provide pension parity between the Chicago Teachers Pension Fund (CTPF) and all other school districts in Illinois. Currently there is an inequitable funding structure under which Chicago taxpayers pay for most of the cost of Chicago teachers’ pensions and also contribute downstate and suburban teachers’ pension costs A more equitable solution could be achieved by either the State assuming responsibility for the unfunded liability of CTPF as it does for all other school districts or a full consolidation of CTPF with the State of Illinois Teachers Retirement System (TRS). This would ease fiscal pressure on the Chicago Public Schools and/or could potentially reduce property tax burden for Chicago taxpayers if the current CPS special pension levy were reduced or eliminated.

- Reduce the number of local governments to eliminate duplicative administrative functions and positions and, correspondingly, cap or reduce property taxes. This could take the form of consolidation, transfer of functions to other governments, or elimination.

- Put a moratorium on unfunded mandates that the State of Illinois imposes on local governments for programs such as employee pension sweeteners, which are funded primarily by property taxes.

- Impose caps on how much local government spending can increase annually.

Conclusion

Property tax limitations can play an important role in moderating tax growth and providing greater predictability for taxpayers, but they are not a cure-all for rising property tax burdens. The reality in Illinois demonstrates that limitations are only as effective as their design and enforcement, and that exemptions, structural inequities, and underlying spending pressures can undermine their intended impact. Meaningful property tax relief will require addressing the root causes of levy growth, including the funding of public education, pension obligations, government fragmentation, and unfunded mandates. Ultimately, policymakers must balance the goal of taxpayer protection with the need to ensure adequate, stable, and equitable funding for the public services that residents rely on.

References

1The discussion of types of property tax limitations is drawn from Janelle Fritts, Property Taxes by State and County, 2026, Tax Foundation, March 16, 2026.

2 Janelle Fritts, Property Taxes by State and County, 2026, Tax Foundation, March 16, 2026.

3 Bethany Paquin. Chronicle of the 172-Year History of State-Imposed Property Tax Limitations. Lincoln Institute of Land Policy. October 2024, p. 4.

4 Measure 50 is paired with Measure 5, passed in 1990, which limits levies to $5 per $1,000 of real market value for school districts and $10 per $1,000 of real market value for general governments. League of Oregon Cities. FAQ on Measures 5 & 50. January 2026.

5 Massachusetts Department of Revenue, Division of Local Services. Levy Limits: A Primer on Proposition 2 ½.

6 Chris Berry, Roland Calia, Eric Langowski, and Annie McGowan. Property Tax Limitations In Practice: What The Data Reveals About Property Tax Caps In Cook County. Civic Federation and Mansueto Institute for Urban Innovation at the University of Chicago Harris School of Public Policy, November 12, 2025.

7 Adam Langley, Bethany Paquin and Yonhui Um, Understanding State Property Tax Limits, Lincoln Land Institute, November 2025.

8 California State Board of Equalization, California Property Tax: An Overview, Publication 29, March 2025.

9 Wisconsin Statutes § 121.91.

10 Elizabeth Ramey, The TABOR Revenue Limit, Colorado Legislative Council Staff, October 11, 2022.

11 Tina Sfondeles and Mawa Iqbal. Bears exit from Chicago closer to reality as House passes bill helping Arlington Heights bid, Chicago Sun-Times, April 23, 2026.