June 11, 2026

by Roland Calia

Chicago's budget debate has increasingly focused on whether the City should adopt stricter standards for structural budget balance and long-term financial planning. New York City provides one example of a major U.S. city operating under a more rigorous legal framework. This report examines how major U.S. cities prepare budgets and compares Chicago’s flexible budgeting with New York City’s stringent budget-preparation requirements.

Accounting Methods Used in Government Financial Reports

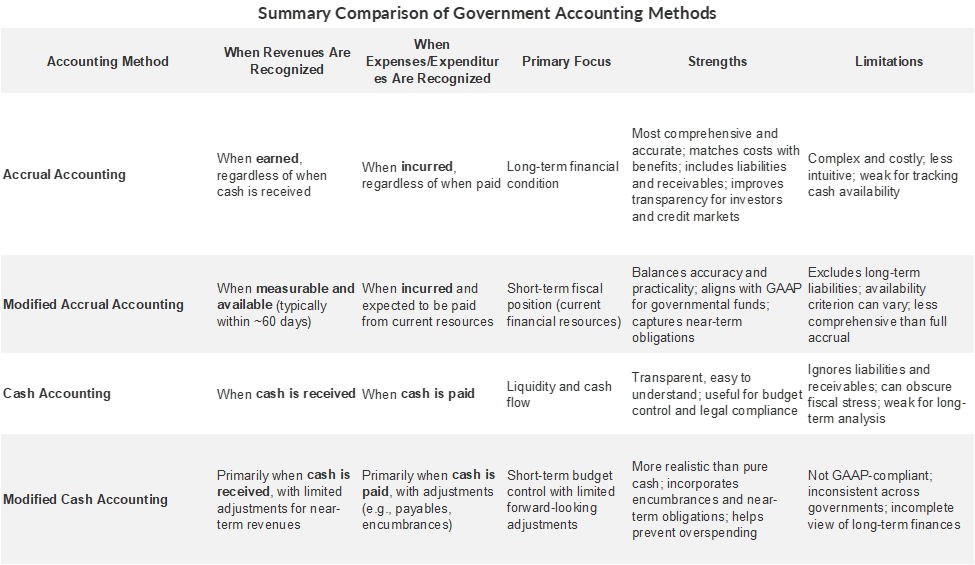

Governments use different bases, or methods, of accounting to record financial transactions. The difference between these methods lies in the timing of transactions and when events are recognized and reported.1

Accrual Accounting

Accrual accounting records transactions when they occur, not when cash is received or paid.

- Revenues are recognized when earned—even if cash is received later (e.g., grants or tax revenue owed but paid months later).

- Expenses are recognized when incurred—when goods or services are received, or obligations arise, regardless of the timing of payments.

- Expenses are matched to the period in which they help generate revenues.

Accrual accounting is used in the private and nonprofit sectors and by some national and local governments. It is used by governments in audited financial reports for government-wide financial statements to capture overall long-term financial position. It is also required for Proprietary Funds (e.g., business-type or enterprise funds) and Fiduciary Funds (e.g., pension funds).

Accrual accounting answers the question: What is the government’s true financial condition?

More specifically, accrual accounting provides a comprehensive and more accurate financial picture than other accounting methods by recording economic activity when it occurs, aligning costs with the periods in which benefits are received, recognizing all revenues and expenses, and including liabilities and earned revenues not yet paid or received. It also improves creditworthiness and helps increase investor confidence in debt issuances.

However, accrual accounting is more complex and costly to manage. It is less useful for tracking available cash in budgeting and is less transparent to non-experts, including elected officials, than cash-based systems.

Modified Accrual Accounting

Modified accrual accounting recognizes revenues only when they are measurable and available, that is, collectible within the current period or soon enough thereafter (often about 60 days) to pay current liabilities. Revenues received within this window are recorded in the current fiscal year, while those received later are deferred to the next period.

Expenditures are recognized when a liability is incurred and expected to be paid from current financial resources. This creates a short-term focus, as obligations are recorded only if sufficient resources are available, making it similar to cash accounting but with limited accrual adjustments.

Modified accrual accounting is used in audited financial reports for the four governmental funds (General, Special Revenue, Capital Projects, and Debt Service) that account for the general operations of a government.

Cash Accounting

Under the cash accounting method, income or revenues are not counted until cash is actually received, and expenses are not counted until they are actually paid. It answers the question: Is there sufficient cash to pay bills that are due?

Cash accounting focuses on short-term cash flow. It is easy to understand and useful for managing annual spending, liquidity, and legal compliance. However, because it often excludes unpaid obligations, it can obscure medium- and long-term fiscal stress from deferred bills and liabilities.

Modified Cash Accounting

This is a hybrid approach commonly used by governments that combines cash accounting with certain limited accrual accounting features:

- Revenues are recorded when cash is received, and expenditures are recorded when cash is paid.

- Short-term expenses (accounts payable) may be recognized when a liability is incurred near the end of the year, even if payment occurs shortly after.

- Encumbrances are recorded when a government issues a purchase order or signs a contract, reserving budgeted funds before cash is paid to prevent overspending.

- Revenues expected very soon after the fiscal year ends (e.g., within 30–60 days) may be recognized in the current budget period.

Modified cash budgeting provides a more realistic picture of short-term finances than pure cash budgeting. However, because it only recognizes certain budgetary adjustments, it provides an incomplete view of long-term liabilities and long-term fiscal conditions. Its use is also not standardized across governments.

Generally Accepted Accounting Principles (GAAP)

The Governmental Accounting Standards Board (GASB) establishes the standard accounting rules, conventions, principles, and procedures that governments use to prepare, present, and report financial information in a consistent, transparent, and comparable way. These standards are referred to as Generally Accepted Accounting Principles (GAAP). GAAPgoverns financial reporting for external financial reports such as Annual Comprehensive Financial Reports (ACFRs) that governments prepare annually after the close of a fiscal year.2

Governmental GAAP is characterized by a fund accounting structure that separates resources into distinct funds (such as the General Fund and Special Revenue Funds) to ensure they are being used legally and appropriately.

What Accounting Methods are Required for Audited Financial Reports?

GAAP requires that government audited financial reports use two accounting methods:

- Full accrual accounting for government-wide financial statements to capture its overall long-term financial position. Accrual accounting is also required for Proprietary Funds (e.g., business-type or enterprise funds) and Fiduciary Funds (e.g., pension funds).

- Modified accrual accounting for the four governmental funds (General, Special Revenue, Capital Projects and Debt Service) that account for the general operations of a government to focus on near-term financial resources and obligations.

What Accounting Methods are Required for Government Budgets?

When preparing budgets, governments can use any of the four following methods: cash accounting, modified cash accounting, accrual accounting and modified accrual basis of accounting or variations of those methods.3

The United Kingdom, Australia and New Zealand4 require that national and local budgets be prepared using accrual accounting. No major US local government prepares an accrual or fully GAAP compliant budget, although many incorporate many or most of GAAP features into their budgets. They typically deviate in some way from full compliance with certain exceptions.

The Governmental Accounting Standards Board does not require accrual accounting for budgeting and recognizes that budgets may be prepared on non-GAAP bases.5 Similarly, the Government Finance Officers Association recognizes that many governments budget on a non-GAAP basis and has not adopted a best practice recommending the use of accrual accounting or GAAP compliant budget preparation.6

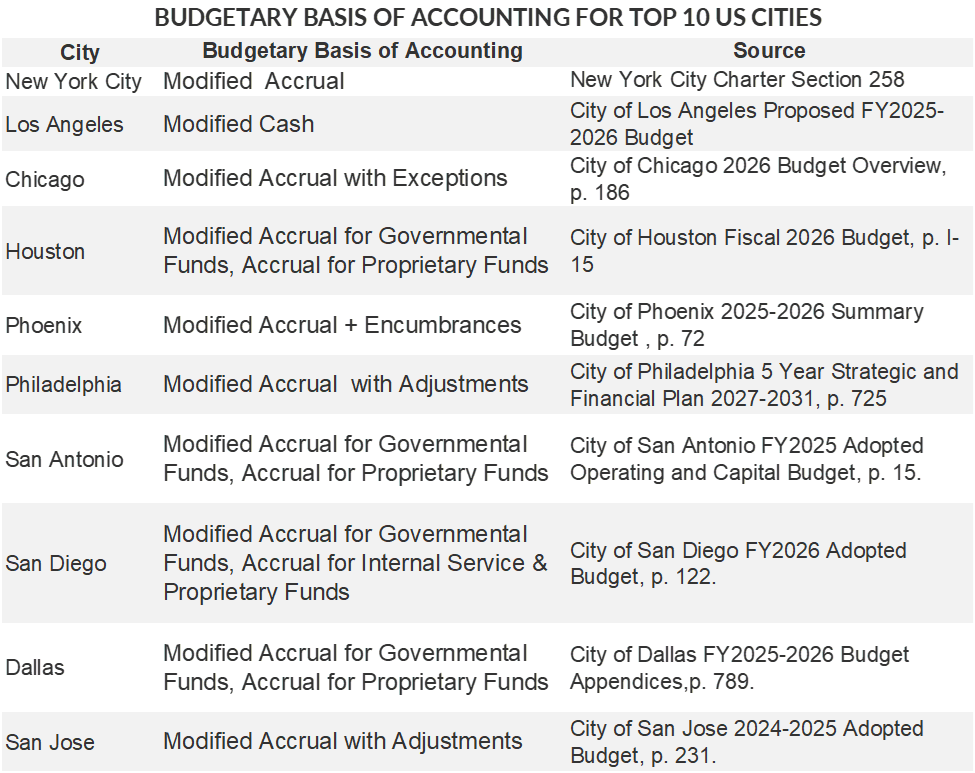

What Accounting Methods Do Major U.S. Cities Use in Their Budgets?

None of the top ten U.S. cities in population use full accrual accounting to prepare their municipal budget and none prepare their budgets in full compliance with GAAP requirements, though their budgets may contain GAAP features. Instead, they use a variety of cash, modified cash and modified accrual bases of accounting.

Local governments’ budgets are often prepared on a budgetary basis that differs from GAAP.7 This budgetary basis is focused on legal compliance, financial control, and short-term resource flows.8 Common differences from GAAP include treating encumbrances as expenditures, expensing capital outlays without depreciation, recognizing debt service on a cash basis, using availability-based revenue recognition, including transfers as inflows/outflows, and excluding long-term liabilities.9 Even where accrual concepts are used (e.g., proprietary funds), non-cash items such as depreciation are often simplified or omitted in budgets.10

The table below shows that:

- The City of Los Angeles uses a modified cash accounting basis to prepare its budgets.

- The other nine cities use modified accrual accounting with differing adjustments or exceptions to develop their governmental funds budgets. Some explicitly note that they use accrual accounting for their proprietary and/or internal service fund budgets.

New York City’s Basis of Budgeting

New York City is required by the New York State Financial Emergency Act (FEA) and the City Charter to adopt a structurally balanced operating budget and a long-term financial plan. The operating budget is developed on a budgetary basis that incorporates modified accrual concepts. The City provides reconciliations between budgetary results and GAAP-based financial statements.11

The City Charter in Section 258 includes strict requirements for how the City plans and manages its finances. Specifically:

- Annual operations cannot show a GAAP deficit unless the deficit is covered by withdrawals from the revenue stabilization fund.

- The mayor must prepare and regularly update a rolling four-year financial plan aligned with these standards.

- Budgets must be structurally balanced (excluding capital items) and consistent with the financial plan, and debt cannot be issued unless it aligns with the plan.

Chicago’s Basis of Budgeting

Chicago uses modified accrual as the basis of budgeting, with the exception of property taxes and Enterprise Funds. For budgeting purposes, property taxes are considered revenue for the year in which the taxes are levied.

Chicago’s operating budget differs from full GAAP compliance in the following ways:

- Encumbrances are budgeted as expenditures. GAAP classifies encumbrances as assigned fund balance.

- Property tax revenue is estimated using a forecasted levy and collection model, rather than waiting for actual collections to occur.

- Long-term debt proceeds and operating transfers are classified as revenues. GAAP classifies these as other financial sources.

- Chicago’s enterprise funds are presented in the budget using a condensed version of accrual accounting, not the full GAAP financial statement presentation found in the ACFR.

- The City does not budget for doubtful accounts. GAAP reports doubtful accounts.

- The City does not budget for in-kind contributions. GAAP classifies in kind donations. received as revenues and those that are used as expenditures.

- The City classifies the prior year’s surplus as an available resource. GAAP records it as a portion of a city’s fund balance.12

Chicago is required by state law to develop a balanced budget.13 However, unlike New York City, there are no legal requirements to balance the operating budget on a structural basis, develop and adhere to a multi-year financial plan, or refrain from issuing debt unless it is in line with a formal financial plan.

References

1 Steven A. Finkler, Thad D. Calabrese, and Daniel L. Smith, Financial Management for Public, Health, and Not-for-Profit Organizations, 8th ed. (Washington, DC: CQ Press, 2025).

2 Financial Accounting Foundation. What is GAAP?

3 Steven A. Finkler, Thad D. Calabrese, and Daniel L. Smith, Financial Management for Public, Health, and Not-for-Profit Organizations, 8th ed. (Washington, DC: CQ Press, 2025).

4 Organization for Economic Co-operation and Development (OECD), Accrual Practices and Reform Experiences in OECD Countries (Paris: OECD, 2017).

5 Governmental Accounting Standards Board, Statement No. 41: Budgetary Comparison Schedules—Perspective Differences—an Amendment of GASB Statement No. 34 (Norwalk, CT: GASB, 2003),

6 Government Finance Officers Association. Basis of Accounting versus Budgetary Basis, March 8, 2019.

7 Governmental Accounting Standards Board, Codification of Governmental Accounting and Financial Reporting Standards, Sec. 2400.

8 Government Finance Officers Association, Best Practice: Establishing the Basis of Budgeting

9 Governmental Accounting Standards Board, Statement No. 34, Basic Financial Statements—and Management’s Discussion and Analysis—for State and Local Governments.

10 Government Finance Officers Association, Best Practice: Budgetary Basis of Accounting.

11 New York State, Financial Emergency Act for the City of New York, N.Y. Unconsolidated Laws § 54(1) and City of New York, New York City Charter, § 258(b). Also New York City Annual Comprehensive Financial Report For the Fiscal Years Ended June 30, 2025 and 2024, p. 98.

12 City of Chicago 2026 Budget Overview, p. 186.

13 See City of Chicago Office of Budget and Management, Budget Information, 65 ILCS 5/8-2-9.1 and 65 ILCS 5/8-2-9.3.