September 07, 2017

For nearly two months, the fate of Illinois’ budget for the current fiscal year was in doubt because of Governor Bruce Rauner’s veto of a school funding bill. With compromise education funding legislation enacted on August 31, attention can now turn to the FY2018 budget itself and specifically on whether it is balanced.

An operating budget is balanced if expenditures match projected revenues. On paper, the budget enacted by the General Assembly on July 7—in an override of another gubernatorial veto—has a modest surplus. However, the Governor and his budget staff have maintained that the legislature’s financial plan for the year that ends on June 30, 2018 is actually in the red.

The issue has heightened importance this year. The General Assembly’s budget attempts to pay down a portion of the State’s multi-billion dollar backlog of accumulated bills, in part by borrowing from capital markets. The operating surplus is needed to pay for borrowing costs.

After initially expressing reservations about the borrowing, Governor Rauner on September 7 said he planned to issue $6 billion in bonds, the maximum amount authorized by the budget legislation. Under the statute, the bonds must be sold by December 31, 2017.

The news release announcing the borrowing plans said the Governor’s Office “is identifying several hundred million dollars in possible spending reductions” to pay for debt service on the bonds.

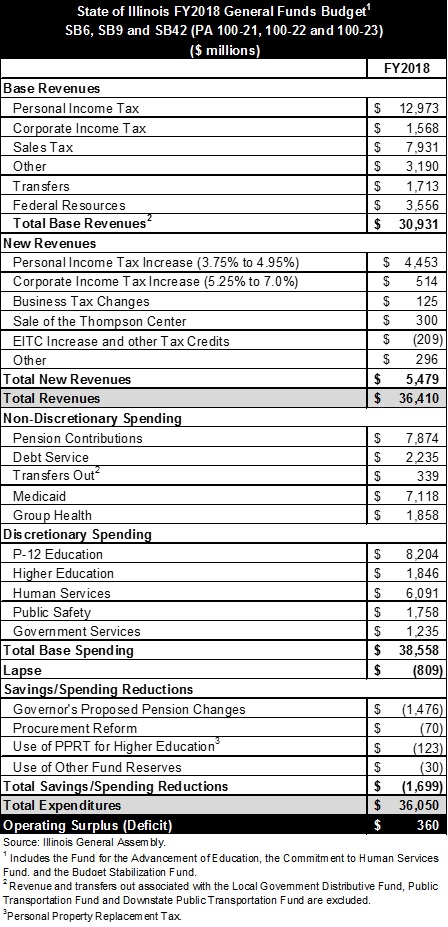

The Governor’s Office has not yet made public a budget grid for FY2018 detailing revenues, expenditures and budgetary balance. The FY2018 budget plan distributed by the General Assembly in July showed general operating revenues of $36.4 billion and expenditures of $36.1 billion. The projected surplus of $360 million amounted to less than 1% of expenditures.

The table below summarizes the legislature’s budget plan.

The narrow surplus shown in the table depends on several uncertain developments. As in the Governor’s proposed FY2018 budget, the legislature’s budget relies on the sale of the James R. Thompson Center in Chicago, with an estimated sale price of $300 million and net proceeds after expenses of about $240 million. The surplus could be reduced if it takes longer than expected to find a buyer or if the structure is sold for less than the projected price.

In its Budget Implementation Act (BIMP), the General Assembly also adopted a pension proposal by the Governor that makes universities and school districts outside Chicago—instead of the State—responsible for pension costs for new employees. The change is expected to save the State $500 million per year, as the reduction in future pension liabilities leads to a sharp decline in current contribution requirements under the State’s funding formula. However, the legislature left timing of the plan’s implementation up to the Teachers’ and State Universities Retirement Systems, raising questions as to how much of the savings will be realized in FY2018.

In addition, the General Assembly’s appropriation bill did not include a required contribution of $11.7 million in FY2018 to the Chicago teachers’ pension fund under Section 17-127 of the Illinois Pension Code. It is expected that this will be funded through a supplemental appropriation.

The education funding legislation enacted in August authorized a five-year pilot program offering up to $75 million per year in income tax credits to individuals or businesses that donate to private school scholarships for low income students. The program does not take effect until the 2018-2019 school year and taxpayers may not take credits for the donations until the tax year beginning on January 1, 2018. Because those returns are filed in 2019, the State apparently will not be affected by the revenue loss until FY2019.

In his veto message on the legislature’s FY2018 budget, Governor Rauner stated that the financial plan was $2 billion out of balance. The news release announcing plans for the bond sale put the operating gap at more than $1 billion.

State budget officials said the deficit estimates covered estimated pension savings as well as certain FY2017 costs, such as day-to-day agency expenses, that have not been accounted for and may need to be appropriated in the FY2018 budget. Although the larger deficit estimate included FY2017 group health insurance costs, the legislature’s budget assumes that these bills will be paid from borrowing.

The State’s accumulated backlog of bills stands at more than $15 billion, according to the Illinois Comptroller’s Office. As discussed here, the General Assembly’s budget did not attempt to address the entire backlog in a single year. Rather, the BIMP authorized a package of measures that sponsors claimed would reduce the accumulated bills by about $8 billion.

Among other provisions, the act authorized up to $6 billion in borrowing from capital markets. However, the small projected budget surplus was estimated to support only $3 billion in borrowing capacity.

According to the Comptroller’s Office, $5.5 billion of the backlog was accruing interest penalties as of June 30. The State pays approximately $2 million per day in interest costs under the Prompt Payment Act, which requires payment of more than 12% interest on some overdue bills, and the Timely Pay provisions of the Insurance Code, which require 9% interest on overdue doctor and hospital bills.

The legislature’s Commission on Government Forecasting and Accountability recently estimated that the State would pay rates between 4.5% and 6.5% on the proposed borrowing to pay down the backlog.

In its FY2018 Roadmap for the State, the Civic Federation endorsed borrowing to pay down the bill backlog in order to save on interest penalties and restore confidence in the State’s finances. The Federation said the borrowing should be paired with a credible plan to balance the budget, accounting for revenues needed for debt service. The Governor and General Assembly should work together to establish the credibility of the surplus so plans for the borrowing can proceed.