December 08, 2009

Facing a multi-billion dollar mountain of unpaid bills and declining revenues, Governor Pat Quinn has proposed a new short-term borrowing plan for the State of Illinois that has encountered opposition from the Comptroller’s Office.

As previously reported in this blog, the Governor in late October announced his intention to borrow $900 million to help catch up on payments to state vendors and service providers. The original plan called for borrowing based on revenue shortfalls, known as “failure in revenues” under the State’s Short Term Borrowing Act. David Vaught, Director of the Governor’s Office of Management and Budget, said in October that personal income tax and gaming tax collections would be $900 million below previous projections. Borrowing based on revenue shortfalls requires repayment within 12 months of issuance. It also requires the Governor to give written notice to the General Assembly and the Secretary of State, explaining the reasons for the borrowing and the measures proposed to restore the State to fiscal soundness.

The State may also engage in short-term borrowing if it faces cash-flow pressures—significant timing variations between disbursement of appropriations and receipt of revenues. In a letter on December 2, 2009 to Illinois Comptroller Dan Hynes, the Governor’s office said it was now planning a $500 million borrowing related to cash-flow problems. Under the new plan, the borrowing would have to be repaid by June 30, 2010, the end of the State’s 2010 fiscal year.

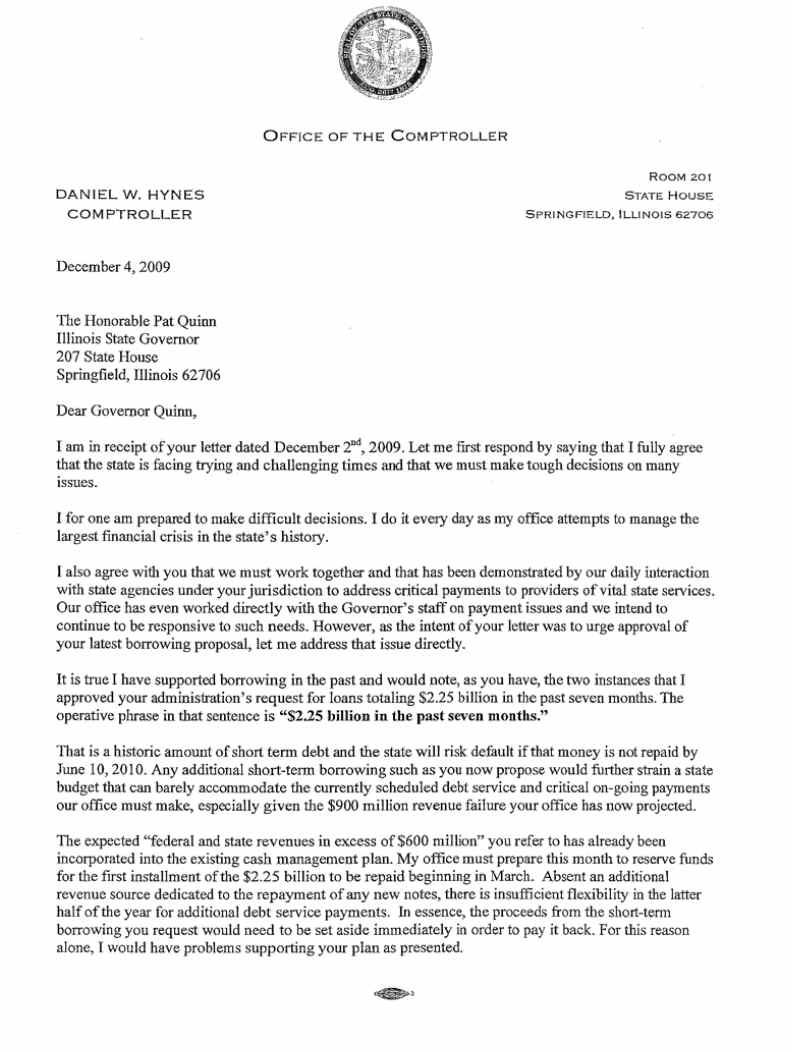

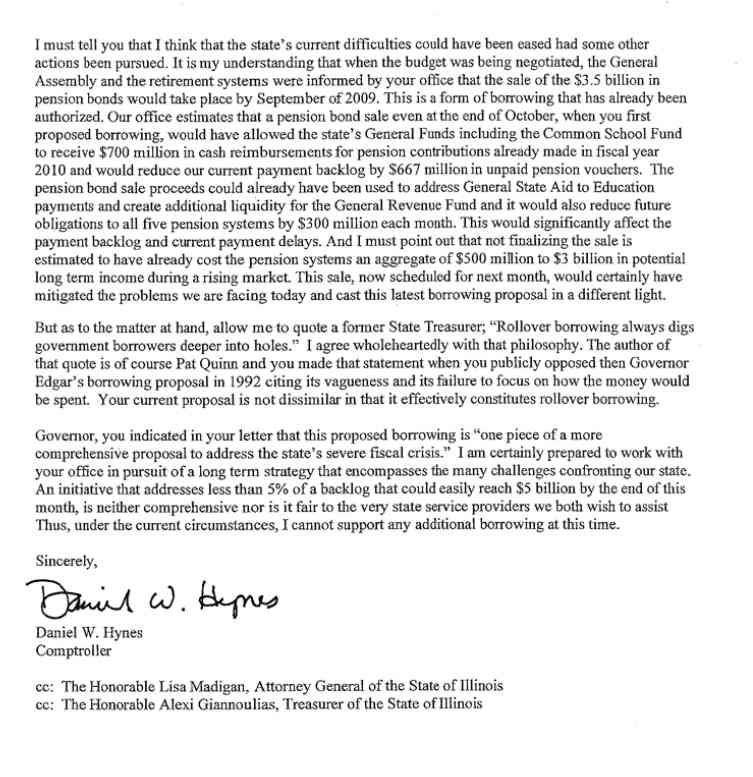

On December 4, Comptroller Hynes responded that he would not approve the request for new short term borrowing [Page 1 and Page 2]. Both the Treasurer and the Comptroller must approve all new state borrowing before bonds can be sold. Comptroller Hynes, who is running against Governor Quinn in the Democratic gubernatorial primary in February, stated in his letter to the Governor that the proposed borrowing “would further strain a state budget that can barely accommodate the currently scheduled debt service and critical on-going payments our office must make.”

{kind=link}

{kind=link}

The Comptroller said in the letter that the Governor’s office could have eased current problems by selling $3.5 billion in pension bonds by September of 2009, as had been previously approved as part of the state’s FY2010 budget. The bonds are intended to finance most of the State’s required FY2010 contribution to employee retirement systems. Comptroller Hynes said a pension bond sale would have allowed the State to immediately reimburse its General Funds for $700 million in pension contributions already made in FY2010 and permitted a $667 million reduction in the backlog of bills. The State’s unpaid bills could reach $5 billion by the end of December, according to the Comptroller’s office. In a separate letter to the State’s service providers, the Comptroller said that the amount of unpaid bills currently stands at $4.4 billion.

The Governor’s position is that the State will receive federal and state revenues of more than $600 million by the end of FY2010 that could be used to pay off the new borrowing. The Comptroller, on the other hand, has stated that the money is not available to repay the proposed borrowing because it has already been incorporated into the existing cash management plan. The State is already obligated to repay $2.3 billion in short-term debt by the end of FY2010. Treasurer Alexi Giannoulias has not yet weighed in on the Governor’s new borrowing plan.