June 22, 2010

The State of Illinois has yet to determine how it will handle its required pension contributions for FY2011. However, a recent analysis by the Commission on Government Forecasting and Accountability (COGFA) estimates that skipping the $3.5 billion payment entirely would cost the State $12.5 billion in additional contributions.

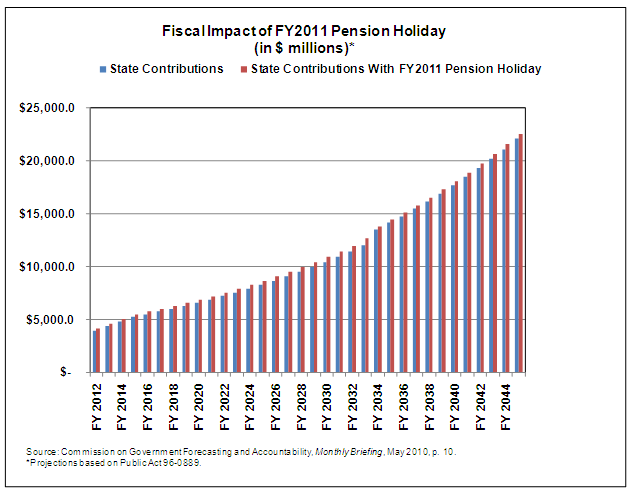

COGFA’s actuaries forecasted how much the State would be required to contribute to its five retirement systems between FY2012 and FY2045 with and without a pension holiday in FY2011, which begins on July 1, 2010. According to the projections, the State would have to pay more every year with the pension holiday in order to reach the 90% funded ratio required by 2045 under state law. The State’s annual contributions would increase every year due to the need to make up for investment income lost during the year when payments were skipped. The following chart shows the results of COGFA’s analysis.

In FY2012, for example, the State’s contributions would total an estimated $3.9 billion with no pension holiday the previous year and $4.1 billion with a holiday. The projections incorporate the impact of Public Act 96-0889, the pension reform measure passed by the General Assembly and signed by Governor Pat Quinn in the spring of 2010. The new law reduces benefits for new employees by raising the retirement age, limiting the maximum pensionable salary and scaling back cost-of-living adjustments, among other provisions.

In light of Illinois’ fiscal crisis, it remains to be seen how the State will deal with required FY2011 contributions, which COGFA estimates at $3.5 billion. When the General Assembly adjourned on May 27, a bill (SB 3514) to issue $4.1 billion in pension obligation bonds had passed the House but not the Senate. Legislation to delay the FY2011 payment (HB 543) had passed the Senate but not the House.

House Bill 543 provides that no retirement systems contributions will be made from the State’s General Funds until the Governor certifies to the Comptroller that adequate funds are available. The bill would amend the State Pension Funds Continuing Appropriation Act, which automatically transfers money into the retirement systems. General Funds support the regular operating and administrative expenses of most state agencies and are the funds over which the State has the most control and discretion. Roughly 90% of state pension contributions come from General Funds.

Under current law, the retirement systems calculate and certify the amounts needed each year to meet the requirements of the statutory funding schedule. Certifications for the next fiscal year must be made by November 15 of the current fiscal year. As a result, the amounts certified by the systems for FY2011 do not reflect the enactment of the pension reform legislation. Certified General Funds contributions for FY2011 total $4.2 billion, according to Governor Quinn’s FY2011 recommended budget.

The State must pursue a new certification in order to reduce contributions in line with the pension reform law. A recertification provision was in the pension borrowing bill that passed the House but not the Senate. As of April of 2010, the Governor’s Office of Management and Budget estimated that the pension reform legislation would reduce the FY2011 General Funds contributions by $382 million. Please see the Civic Federation’s analysis of the Governor’s FY2011 recommended budget for more information on the State’s retirement systems.