April 29, 2010

The Civic Federation recently released its analysis of Governor Pat Quinn’s recommended FY2011 operating and capital budgets for the State of Illinois. One of the Federation’s strongest points of opposition to the proposed $52 billion operating budget was that it relied heavily on borrowing for operations.

The budget as proposed by the Governor called for borrowing to fund $4.7 billion of the total $32.1 billion needed for operating expenditures in FY2011. Recently the Governor increased the suggested borrowing to $5.7 billion in operating debt, which now specifically includes selling pension obligation bonds (POB) to pay the majority of the State’s required contribution to its retirement systems for FY2011.

The original budget proposed by the Governor on March 10, 2010 described borrowing for operations as “voucher payment notes.” There is currently no provision in the Illinois Bond Authorization Act to provide for this type of borrowing and no details were provided in the budget regarding the term of the debt, cost of the issuance or type of authorization the State would need to enact to issue this new debt to fund operations. The FY2011 budget book simply defines the voucher payment notes as “a series of notes to pay specific vouchers during the fiscal year.”

On April 20, 2010, the Governor’s Office of Management and Budget provided further information on a revised budget proposal from the Governor, which included a possible income tax increase and increased total borrowing for operations in FY2011 to $5.7 billion. The new plan specified three types of debt including:

- Private placement pension notes totaling $3.7 billion;

- Borrowing $1.0 billion from “rainy day funds;” and

- Securitizing part of the State’s Tobacco Settlement revenue to borrow $1.0 billion.

As previously discussed on this blog, the Civic Federation disagrees with the notion that selling debt to support the State’s operating cost is a sustainable or prudent source of annual operating revenue or a solution to the State’s deficit. Debt is a onetime revenue source that increases the cost of future operations. By funding current operations through debt, the State complicates future budgets in two distinct ways. First, the debt service required for repayment of the loans increases the strain on the subsequent operating budgets. This means that the State has to find a way to fund the repayment of the debt beginning the year after it is issued when its expenditures already exceed anticipated revenues. Second, the State will begin the following fiscal year with a hole in its operating revenues at least the size of the amount it borrowed for operations in the previous fiscal year.

The proposed “rainy day fund” borrowing from the State’s other special funds may be less costly than selling debt on the municipal bond market. In the past the Civic Federation has supported sweeping excess funds from these accounts and eliminating or consolidating as many of the over 600 special state funds as possible. However, if the State must pay back the money borrowed from these accounts in the next fiscal year, it would still face the problem of the budget short fall in FY2012 and not have not necessarily have that revenue available in the following year.

Securitizing the revenue the State receives from the settlement of its liability lawsuit against the tobacco industry does have the benefit of not increasing the strain on the operating funds to pay back the loan. However, the $1 billion in funding from the loan will not be available as revenue in the next fiscal year. In addition, some or all of the annual tobacco settlement payments to the State, which average around $300 million, would be pledged to repay the loans. This would mean any programs currently funded with settlement funds would have to be funded by another source or cut. Together the tobacco settlement borrowing and rainy-day fund borrowing alone would create at least a $3 billion budget hole going in FY2012.

Any debt issued used to pay for current year operations that is not paid back within the same fiscal year results in a payment of future General Funds for current operations and limits what the State will be able to afford for years to come.

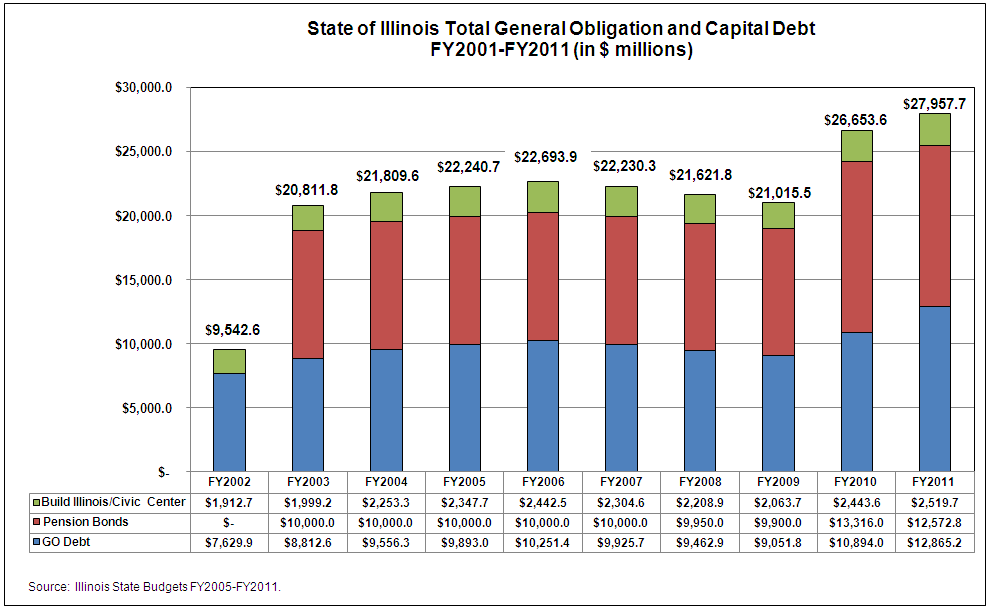

The Civic Federation continues to oppose issuing more debt to fund the pensions because it is not sustainable and the contribution increases every year. The State of Illinois cannot afford to continue to issue pension obligation bonds (POB), as it did in FY2003 and FY2010, and which now makes up nearly half of the State’s total debt burden. Issuing POBs also increases the cost of funding the pensions by adding debt service on the bonds to the total cost of funding the retirement systems, which the State already cannot afford. The following graph shows the total State debt growth between FY2002 and FY2011 before the sale of any additional debt to support the FY2011 operating budget.

If the State issued the proposed $3.7 billion in new FY2011 POBs, the total debt burden would grow to $31.7 billion, of which 51.4% would be from pension borrowing alone.

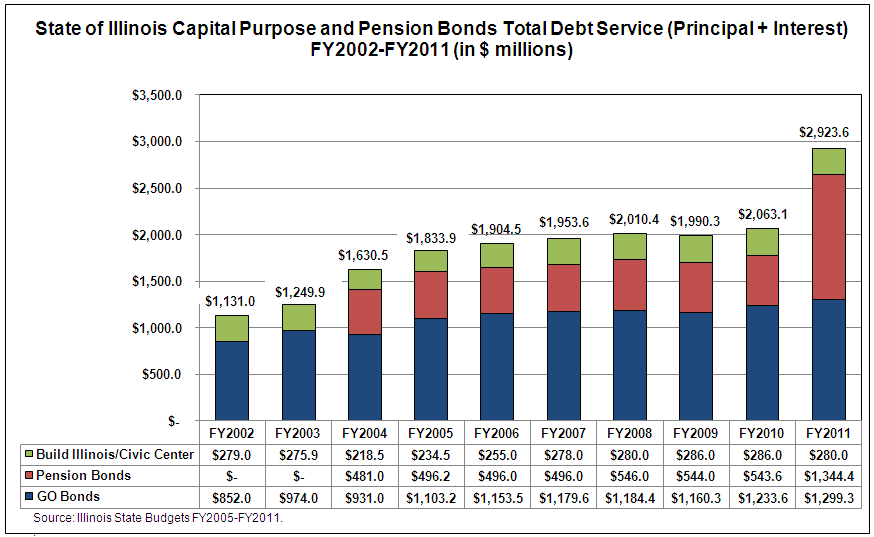

The strain of borrowing for operations on the State’s budget is evident when looking at the increase in debt service the State will pay in FY2011 after it sold $3.5 billion in POBs in FY2010. The following graph shows the updated total debt service for the State of Illinois included in the FY2011 budget.

Debt service owed by the State increased 41.7% from FY2010 to FY2011 due almost entirely to the issuance of additional POBs. Similarly the State saw a 30.5% increase in annual debt service in FY2004 after the sale of $10 billion in POBs in FY2003. The FY2010 pension debt will be paid back over five years whereas the FY2003 issuance was financed over 30 years. In all, the State is on the hook to pay a total of $9.4 billion in interest on $13.4 billion in pension bonds outstanding between FY2010 and FY2033. It is unclear how much an additional $3.7 billion issuance would affect the total debt service owed because the Governor has yet to reveal the term of the debt or anticipated interest rate.

The Debt Trends section of the Civic Federation’s full analysis of the FY2011 capital and operating budgets, which begins on page 66, discusses in further detail issues regarding the State’s overall debt profile and growing debt burden.