January 27, 2011

In discussions of the State of Illinois’ budget, no issue is more contentious—or more confusing—than recent spending trends. Simply stated, is Illinois spending more or less than it was two years ago?

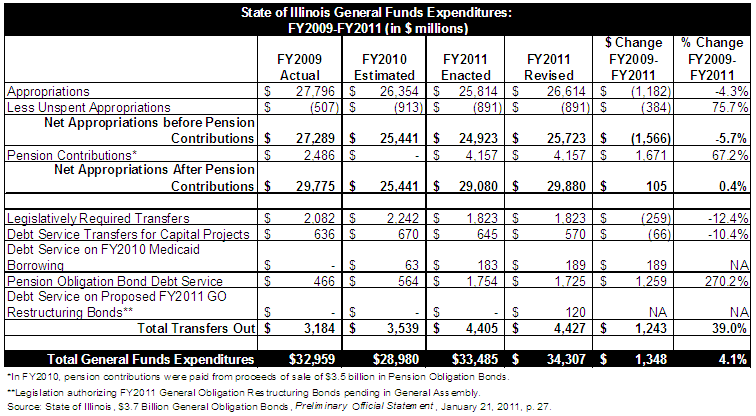

As previously indicated on this blog, the answer depends on what is meant by spending. According to preliminary information (available at MuniOs.com) provided by the State on January 21, 2011 in connection with an upcoming bond sale, General Funds appropriations are projected to decline by $1.2 billion from FY2009 to FY2011. However, the decline in appropriations is more than offset by an increase in total expenditures. Total expenditures—including pension contributions and debt service payments as well as appropriations—are projected to increase by $1.3 billion.

General Funds support the regular operating and administrative expenses of most state agencies and are the funds over which the State has the most discretion and control. For each fiscal year, beginning on July 1, the General Assembly passes and the Governor signs a budget that provides spending authority through appropriations for state activities such as education, healthcare and human services. Existing statutes require additional expenditures for pension contributions, interest and principal payments on outstanding bonds and payments to local governments.

The FY2011 budget as enacted on July 1, 2010 set appropriations at $25.8 billion. Now, as shown in the table below, FY2011 appropriations have been increased by $800 million to $26.6 billion, which represents a decline of 4.3% from $27.8 billion in FY2009. The Governor’s Office of Management and Budget (GOMB) said that the FY2011 appropriations increase reflects a supplemental appropriation to pay Medicaid bills and cover certain other unspecified shortfalls.

A supplemental appropriation represents additional spending authority granted by the General Assembly following passage of the initial budget. The State wants to pay Medicaid bills during FY2011, while Illinois and other states continue to receive enhanced federal funding for the joint federal-state program under the American Recovery and Reinvestment Act of 2009. The enhanced funding is scheduled to end on June 30, 2011. The revised estimate of FY2011 appropriations is now slightly higher than FY2010’s appropriation of $26.35 billion.

According to the revised state numbers, total expenditures are projected to increase by 4.1% from $33.0 billion in FY2009 to $34.3 billion in FY2011. The major spending increases during the period involve higher statutorily required contributions to the State’s underfunded retirement systems and debt service on Pension Obligation Bonds (POBs) issued to make pension payments for FY2010. To pay the roughly $4 billion in pension contributions for FY2011, Governor Pat Quinn on January 14, 2011 signed Public Act 96-1497, authorizing the sale of additional POBs.

The Governor is also supporting a plan to issue $8.75 billion in 15-year General Obligation Restructuring Bonds to help pay down the State’s backlog of obligations, including unpaid bills, employee health insurance claims and corporate income tax refunds. This plan is now pending in the General Assembly as Senate Bill 3. FY2011 expenditures in the table above include debt service on the proposed GO Restructuring Bonds. According to the bond documents, the Governor would use roughly $4.4 billion of the bond proceeds to pay down an estimated $6.4 billion of unpaid bills at the end of FY2011.

Governor Quinn’s budget plan for the next three years was made available to the public on January 20, 2011. Public Act 96-1354, signed on July 28, 2010, requires GOMB to post on its website by January 1 of each year its fiscal policy intentions for the upcoming fiscal year and the next two fiscal years. The budget plan incorporates the increases in personal and corporate income tax rates that took effect on January 1, 2011 under Public Act 96-1496. As previously outlined on this blog, the personal income tax rate rose from 3% to 5% on January 1 and the corporate tax rate rose from 4.8% to 7% and remain in place until January 1, 2015. After that, the personal income tax will be set at 3.75% until 2025 and then drop to 3.25%; the corporate income tax will be set at 5.25% until 2025 and then return to 4.8%. Corporations in Illinois also pay a 2.5% Personal Property Replacement Tax.

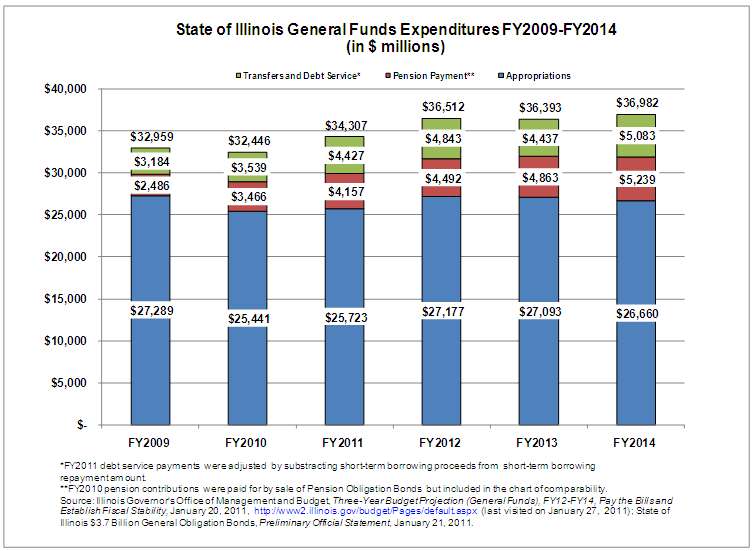

The next chart shows GOMB’s appropriation and expenditure projections from FY2012 through FY2014 under the three-year plan. GOMB’s expenditure projections include debt service payments on the proposed GO Restructuring Bonds. It should be noted that debt service payments for FY2011 were adjusted in the chart to subtract short-term borrowing proceeds from repayments. FY2010 pension contributions in FY2010 were made from the sale of POBs but are included in the chart as expenditures for comparability purposes.

The chart shows appropriations rising by $1.5 billion, or 5.7%, to $27.2 billion in FY2012 from $25.7 billion in FY2011. Total expenditures increase by $2.2 billion, or 6.4%, to $36.5 billion, reflecting increased pension and debt service payments as well as the increased appropriations. The Governor is scheduled to announce details of his FY2012 recommended budget on February 16, 2011.

Expenditure levels in the Governor’s three-year plan decline slightly to $36.4 billion in FY2013 and reach $36.98 billion in FY2014. Total spending would increase by 7.5% from FY2011 to FY2014. Spending levels in the plan do not exceed the expenditure limits established in Public Act 96-1496. The spending caps are: $36.8 billion in FY2012; $37.6 billion in FY2013; and $38.3 billion in FY2014.